LONDON: Successful investors are always looking to get on the right side of an uneven bet, and the shipping market has had an uneven look to it so far in 2015. There has been some improvement in earnings, and the Clarksea Index has risen to around 30% above its 2014 average. However, the upside has not been spread equally across the sectors at all, and the same could be said of trends in capacity growth.

Uneven Territory

Looking at the key markets, the LPG sector has continued to be a star performer, and tankers have had a great run in the year to date too. Containerships have seen charter earnings increase from historical lows, but poor old bulkers continue to see rock bottom levels. It’s an uneven picture to say the least. However, one factor that appears to be more even is the volume of capacity entering the fleet.

Flattening Out

Shipyard output looks fairly steady, with the 6-month moving average of deliveries averaging around 7-8m dwt per month for about a year and half now. As a result fleet growth has slowed from the c.9% level seen in 2010-11, and today the projection is for a fairly steady rate of growth in total cargo fleet capacity, with expected expansion of 3.5% this year and 4.1% in 2016. Is this good news? A high level view may suggest that, with a fair wind on the demand side, more moderate supply side growth at least should not make the underlying market surplus any worse. However, looking in more detail it is clear that the rate of capacity growth is highly uneven across sectors too.

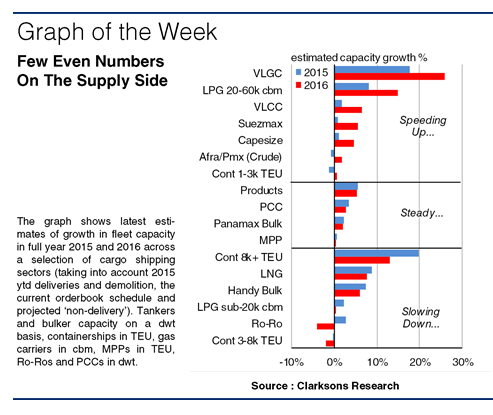

Speeding Up

Supply growth in the key cargo vessel sectors can be split into three. In the fast lane we have those sectors where fleet growth is expected to speed up in 2016. LPG carrier capacity growth already looks rapid (VLGC capacity is projected to grow by 18% this year) and will accelerate again next year. Crude tanker fleet growth will also speed up (VLCC capacity is projected to expand by 6% in 2015). What sort of ‘landing’ might that bring for these markets? Capesize bulker fleet growth will ramp up to 5% in 2016 (as if this sector needed any more pressure), and after a few years of shrinkage the 1-3,000 TEU boxship sector will at last see some (much needed) expansion (1%).

Slowing Down

Supply growth in other sectors looks set to remain relatively steady in 2016 compared to 2015, but there are also a number of sectors where it is projected to slow in 2016. LNG carrier and Handy bulker supply growth will start to recede. Notably, expansion in the large (8,000+ TEU) boxship sector will begin to slow (20% in 2015 to 13% in 2016) whilst the medium-sized boxship fleet will staunchly continue to decline (by 2% in 2016).

So, market earnings are uneven today and despite the big picture suggesting that capacity growth will remain moderately steady across 2015 and 2016, delving into the detail suggests that supply-side impetus will be uneven from one sector to another. Some sectors might be start to feel fresh pressures whilst others might breathe a sigh of relief.—– source Clarksons