KARACHI: Directorate-General Customs Valuation Director Shafiq Ahmad Latki revised customs values of skimmed milk and instant milk powder through Valuation Ruling No. 1430/2019.

Earlier customs values of aforementioned items were determined through Valuation Ruling No. 1329/2018 dated 31.1.2019. The values given in the valuation ruling, being tool, old needed re-determination because the said values did not reflect true prevailing prices in international markets.

Therefore Directorate General Customs Valuation initiated an exercise for determination of the customs values of skimmed milk powder in terms of Section 25-A of the Customs Act, 1969. Meeting with stakeholders including importers was held on 19.11.2019, to discuss the current international prices of the subject goods.

The stakeholders were requested to submit following documents before or during the course of stakeholders meeting so that customs values could be determined:

I Invoices of imports during last three months showing factual value.

Websites, names and e-mail address of known foreign manufacturers of the item in question through which the actual current value can be ascertained.

iii. Copies of contracts made/LCs opened during the last three months showing the value of item in question.

- Copies of contracts made/LC opened during the last three months showing the value of item in question.

- Copies of sales tax invoices issued during last four months showing the difference in price (excluding duty and taxes) to substantiate their continent.

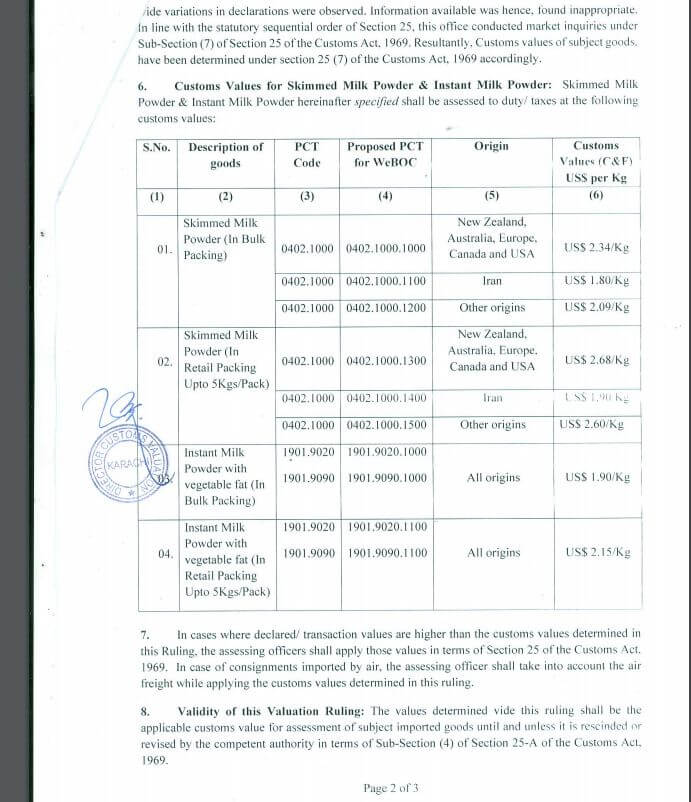

The participants mostly agreed that the prices of subject commodities have shown upward trends in international markets. When enquired if there was any accredited publication which depicts international values, the response of the participants was in negative.

The participated stated that mostly skimmed milk imported in bulk and is used mainly in preparation of confectionery items. Valuation methods provided in Section 25 of the Customs Act, 1969 were duly applied in their regular sequential order to arrive at customs values of subject goods.

The transaction value method as provided in sub-section (I) of Section 25 of the Customs 1969 was found inapplicable due to wide variation of values displayed in the import data.

Thereafter, identical/similar goods value methods as provided in sub-section (5_ & (6) of Section 25 ibid were examined for applicability in the valuation issue in the instant case.