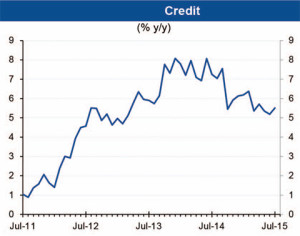

KUWAIT: Credit down in July, though growth rose to 5.5% y/y on basis effects. Total credit declined by a net KD 133 million during the month. The main source of weakness in July was a drop in lending for securities purchases, which reversed a large gain the month before. Nonbank credit also saw a larger decline than usual. These were partly offset by relative strength in household borrowing, and lending to the real estate and trade sectors. Private deposits saw large withdrawals on the month, with money supply growth picking up despite the decline. Meanwhile, interbank and deposit rates held steady.

Despite the weaker July credit figures, we still appear to be seeing an accelerating growth trend since the start of 2015; annualized growth in total credit during the three months through July stood at 6.9% compared to a low of 2.2% in December 2014.

Household borrowing growth remained healthy, though the monthly gain of KD 79 million was slightly weaker than recent trends. Still, growth accelerated to 12.5% y/y. The monthly gain came from installment loans, while consumer loans saw a small decline. Household borrowing remained the largest contributor to credit growth in 2015, accounting for more than half of the gains.

Credit to non-bank financial companies saw a relatively large decline, closing KD 69 million, the largest in 18 months. The sector’s credit was down 10.3% y/y.

All remaining credit declined by KD 143 million, though growth rose to 3.4% y/y. The bulk of the decline was in lending for the purchase of securities, which was down by KD 222 million. Gains in the trade, real estate, and construction sectors helped offset some of the decline. Taken alone, business credit excluding securities saw a healthy gain, with credit growth rising to 4.5% y/y.

Private deposits saw a large KD 453 million decline in July. This was likely due to the summer travel season, though the decline was smaller than last year’s. Money supply (M2) growth still rose to 4.7% y/y. The decline in deposits was in both dinar (-KD 315 million) and foreign currency deposits (-KD 138 million). There was also a move away from KD sight and savings deposits towards KD time deposits. Narrower money supply (M1) was still down 0.6% y/y due to a basis effect as a result of last year’s introduction of the new paper currency, which temporarily increased the amount of currency in circulation.

Average customer deposit rates on dinar time deposits, and interbank rates were steady in July. Average rates onthe1-month, 3-month, and 6-month time deposits were steady at 0.61%, 0.77%, and 0.97%, while 12-month rates added one basis point to settle at 1.21%. KD interbank rates held steady at1.00%, up 21 basis points year-to-date.